Nvidia’s unveiling of its next‑generation Vera Rubin AI platform sent Asia’s chipmakers soaring before a fresh US export‑permit threat triggered a sharp pullback. Taiwan’s TSMC, Korea’s Samsung and SK Hynix jumped 5–8 per cent on news that Rubin would use even more advanced HBM4 memory and 2nm processes, only to shed most gains after Washington signalled tighter licensing for high‑end AI accelerators to China.

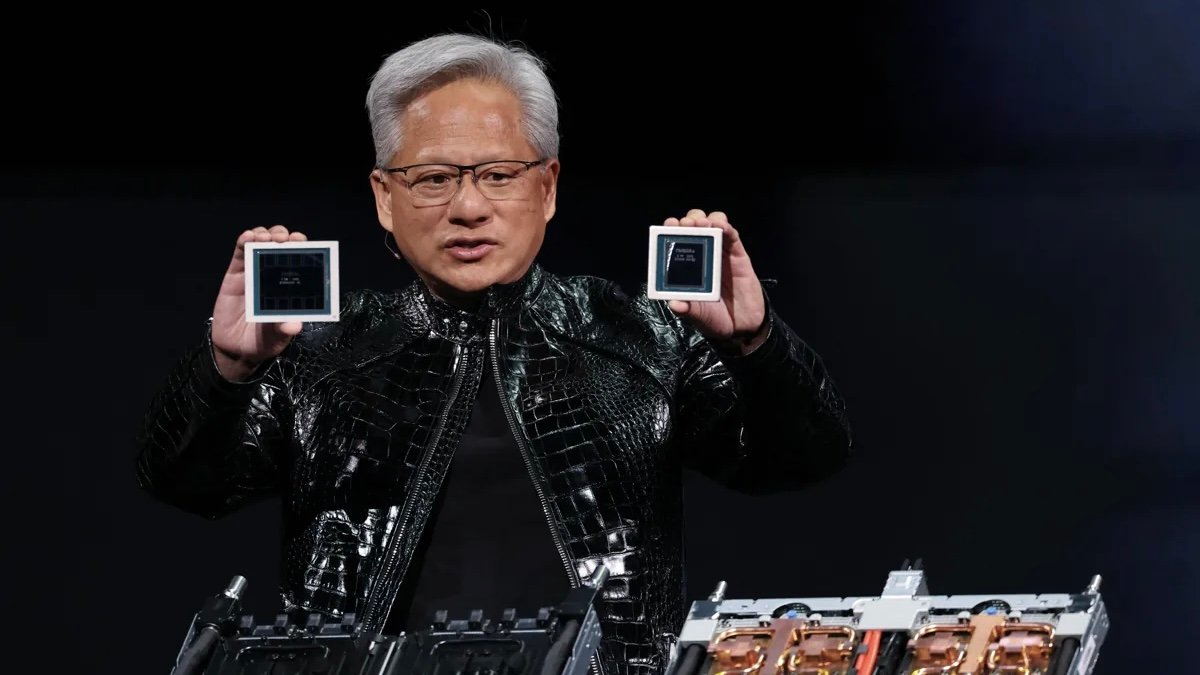

Rubin, slated for 2027 production, promises 3.3 petaflops performance and 141 billion transistors, requiring HBM4 stacks that only Asian memory giants can supply at scale. Nvidia CEO Jensen Huang confirmed TSMC’s 2nm role and SK Hynix’s exclusive HBM4 partnership. The endorsement validated Asia’s lead in AI hardware manufacturing amid US design dominance.

The rally reflected supply‑chain tightness. HBM3e remains sold out through 2027. Rubin’s power demands will push HBM4 to 16‑hi stacks by 2028. Samsung accelerated HBM4 certification for Q4 2026. TSMC’s CoWoS packaging capacity books full through 2028.

Then came the policy whiplash. US Commerce Secretary Gina Raimondo announced “enhanced review” for AI chips with over 3,000 teraflops performance, effectively targeting Nvidia’s H100 successors destined for China. Permits now required case‑by-case, extending approval times from weeks to months. TSMC warned of US$1.5 billion revenue hit. Samsung flagged China memory sales exposure at 15 per cent.

Markets reacted violently. Hang Seng Tech plunged 4 per cent. Kospi chip index fell 3.5 per cent. Taiwan Weighted shed 2.8 per cent. Beijing vowed retaliation via rare earths and antimony export bans.

Geopolitical risk pricing returns. Taiwan Strait tensions, US election rhetoric and Iran conflict amplify semiconductor volatility. Asia fabs represent 90 per cent advanced capacity, creating mutual dependencies.

Analysts see short‑term pain, long‑term gain. Morgan Stanley cuts TSMC target 10 per cent but maintains overweight. China builds domestic HBM via CXMT and YMTC. Samsung diversifies to automotive and HPC markets. The episode highlights Asia’s semiconductor dilemma: indispensable to global AI yet perpetually vulnerable to Washington’s security hawks. Rubin’s technical brilliance underscores the region’s manufacturing moat, but export controls remind that geopolitics sets the rules. Investors must price both the AI megatrend and the weaponisation risk.